💼 Small Business Guide

🇺🇸 Built for U.S. Consumers

💰 Cost Considerations

Dental Insurance for Small Business Owners: Coverage for You and Your Employees

Running a business means managing many responsibilities, including your health and dental care. Learn how small business owners can compare dental plans, understand coverage options and choose benefits that fit their needs and budget.

🟢What You’ll Learn

In this guide, you’ll learn why dental coverage matters for small business owners, which plan options may be available and what factors to compare before enrolling.

Small business owners often focus on growing their companies, serving customers and managing daily operations. However, dental health remains an important part of overall well-being. Unlike employees who may receive dental benefits through an employer, many business owners must evaluate coverage options independently.

💡Understanding available dental plans can help you make informed decisions about both preventive care and future dental expenses.

For a broader look at how dental coverage priorities may change based on family, age and work situation, start with our guide to dental insurance by life stage.

Why Dental Coverage Matters For Small Business Owners

Good oral health supports overall health and can help reduce the risk of more complex dental problems later.

Many business owners rely on:

- Preventive care

- Routine cleanings

- Exams and X-rays

- Fillings

- Crowns

- Major dental procedures

💡Regular dental care may help identify potential issues before they become more costly to treat.

Do You Need Individual or Small-Group Dental Coverage?

The first step is determining who needs coverage.

A business owner without eligible employees generally looks for individual or family dental coverage. This may apply to a sole proprietor, freelancer, independent contractor or owner whose only other worker is a spouse.

A small business with eligible employees may also be able to consider small-group dental coverage. Group coverage introduces additional questions about employee eligibility, employer contributions, participation requirements, enrollment and plan administration.

Coverage for the Owner Only

Individual dental coverage may be more relevant when the plan is intended only for:

- The business owner

- The owner and a spouse

- The owner and dependent children

- A household without eligible non-owner employees

Review our Dental Insurance for Self-Employed Individuals guide when you are arranging coverage for yourself or your family rather than offering employee benefits.

Coverage for Employees

Small-group coverage may be relevant when the business has eligible employees and wants to offer dental insurance as an employee benefit.

Before comparing group options, determine:

- How many employees are eligible

- Whether coverage will be offered to full-time employees only

- How much of the premium the business may contribute

- Whether employees may enroll dependents

- What participation requirements apply

- How new employees become eligible

- How enrollment and renewal will be administered

Owning a business does not automatically make group dental coverage the appropriate option. The correct structure depends primarily on who will be covered.

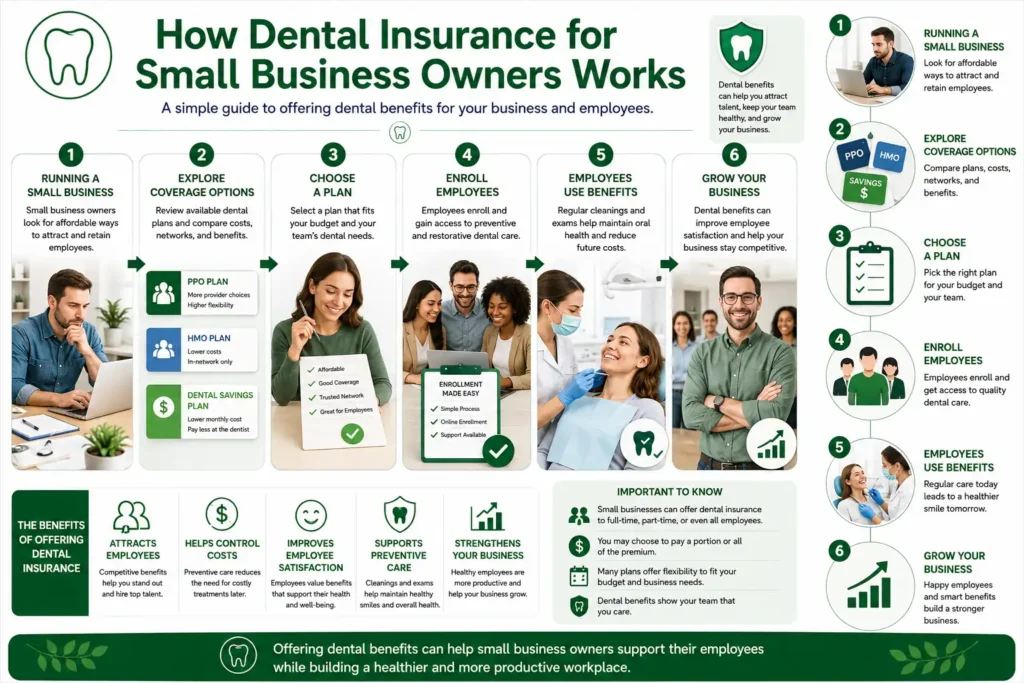

How Dental Insurance for Small Business Owners Works

A simple guide to offering dental benefits for your business and employees.

1️⃣-Running a Small Business

Small business owners look for affordable ways to attract and retain employees.➡️

2️⃣-Explore Coverage Options

Review available dental plans and compare costs, networks and benefits.➡️

3️⃣-Choose a Plan

Select a plan that fits your budget and your team’s dental needs.➡️

4️⃣-Enroll Employees

Employees enroll and gain access to preventive and restorative dental care.➡️

5️⃣-Employees Use Benefits

Regular cleanings and exams help maintain oral health and reduce future costs.➡️

6️⃣-Grow Your Business

Dental benefits can improve employee satisfaction and help your business stay competitive.😁

🦷Attracts Employees 💰Helps Control Costs 😊Improves Employee Satisfaction 🛡️Supports Preventive Care 📈Strengthens Your Business

🟢Dental Coverage Options for Small Business Owners

Small business owners may have more than one way to arrange dental coverage, depending on whether the coverage is only for the owner and family or also for eligible employees.

The right option depends on the size of the business, employee eligibility, budget, provider access and how much administration the business is prepared to manage.

Individual or Family Dental Insurance

Individual or family dental insurance may be more suitable when the business has no eligible employees and the owner needs coverage only for themselves, a spouse or dependent children.

This may apply to:

- Sole proprietors

- Freelancers

- Independent contractors

- Business owners without eligible employees

- Owners whose only other worker is a spouse or family member

When comparing individual or family coverage, review:

- Monthly premiums

- Individual and family deductibles

- Annual maximums

- Waiting periods

- Provider networks

- Dependent eligibility

- Orthodontic benefits, if children may need braces

- Coverage for major services such as crowns, dentures or implants

Review our Individual vs Family Dental Plans guide when deciding whether separate individual coverage or a family plan better fits your household.

Small-Group Dental Insurance

Small-group dental insurance may be relevant when a business has eligible employees and wants to offer dental benefits as part of an employee benefits package.

Compared with owner-only coverage, group dental coverage can introduce additional decisions, such as:

- Which employees are eligible

- Whether dependents can be added

- How much the business will contribute toward premiums

- Whether employees must contribute to their own coverage

- Whether the plan has participation requirements

- How new employees become eligible

- Who manages enrollment and renewals

- Whether the provider network works for employees in different locations

Small-group coverage should be evaluated as both an employee benefit and a business cost.

A plan that works well for the owner may not be the best fit for the entire team if employees cannot easily access participating dentists.

SHOP Dental Coverage

Eligible small employers may be able to offer dental coverage through the Small Business Health Options Program, also known as SHOP.

Eligible small employers may be able to add dental coverage to a SHOP insurance offer or offer a stand-alone SHOP dental plan without offering a SHOP health plan. Some SHOP health plans may also include dental benefits.

As with SHOP health plans, employers can choose how much of an employee’s dental premium they pay.

SHOP insurance is generally available to small employers with 1–50 employees, although requirements can vary by state and situation.

Before considering SHOP dental coverage, confirm:

- Whether the business is eligible

- Whether the business has at least one eligible employee who is not the owner, spouse, partner or family member

- Whether coverage must be offered to all full-time employees

- What employee participation rules apply

- Whether the desired dental plans are available in the business’s state

- How employer contributions are handled

- Whether enrollment is completed through an insurer, agent or broker

- How employees receive plan documents and enrollment support

SHOP dental coverage may be useful for some small employers, but it is not automatically the best option for every business.

Review the current plan details, state availability and employer requirements before making a decision.

Review the official SHOP dental coverage information for small employers.

Coverage Through a Professional Association

Some professional associations, trade groups or membership organizations may offer access to dental coverage or dental discount arrangements for eligible members.

This option may be worth reviewing if the business owner belongs to an industry group or professional organization.

Before enrolling, confirm:

- Whether the option is dental insurance or a discount arrangement

- Who underwrites or administers the coverage

- Whether membership fees are required

- Which dentists participate

- Whether dependents can be added

- Whether employees can participate

- Which services are covered or discounted

- Whether waiting periods, annual maximums or exclusions apply

Do not assume that association-based coverage is available to every small business owner.

The value depends on the specific organization, plan structure, provider network and expected dental needs.

Dental Savings Plans for the Owner

A dental savings plan may be considered when the business owner is looking for an option for themselves or their household rather than an employee group benefit.

Dental savings plans are not insurance. They generally provide access to discounted fees from participating dentists instead of paying claims.

This type of option may be worth comparing when:

- The owner’s preferred dentist participates

- Immediate dental treatment is needed

- Available insurance options have long waiting periods

- Expected treatment is excluded or limited by insurance

- The discounted cost is competitive

- The owner does not need to offer employee benefits

Before joining a dental savings plan, verify:

- The annual membership cost

- The participating dentist list

- The discounted fees for expected services

- Whether specialists participate

- Whether the plan applies to family members

- Whether discounts can be used for major procedures

Dental savings plans may help some owners reduce dental costs, but they do not replace a small-group employee benefit.

Review our Dental Insurance vs Dental Savings Plans guide before comparing insurance coverage with discount-based alternatives.

What Small Business Owners Should Compare

A dental plan should work for both the business and the employees expected to use it.

Before selecting coverage, compare employee eligibility, business contributions, participation requirements, provider access, covered services, plan limits and the administrative responsibilities involved in maintaining the benefit.

Do not evaluate a plan only by its advertised monthly premium. A lower-cost option may provide a smaller provider network, lower annual maximums or more restrictions on major dental services.

Employee Eligibility

Start by confirming exactly who can enroll in the plan.

Questions to ask include:

- Which employees are eligible?

- Are benefits limited to full-time employees?

- Can part-time or seasonal employees enroll?

- When do new employees become eligible?

- Can employees add a spouse or dependent children?

- Are owners, partners or family members treated differently?

- What happens when an employee changes hours or employment status?

For general SHOP eligibility, HealthCare.gov says a business must usually have between 1 and 50 full-time-equivalent employees and at least one eligible employee who is not an owner, partner, spouse or family member of an owner. SHOP employers generally must offer coverage to all full-time employees, while offering it to part-time employees is optional. State and plan rules can differ, so eligibility should always be confirmed before enrollment.

Eligibility rules should be documented clearly so employees understand when coverage begins and who may be included.

Employer Contributions

Decide how much, if anything, the business will contribute toward employee premiums.

The business may need to consider:

- The amount contributed for each employee

- Whether employees pay part of their own premium

- Whether the business contributes toward dependent coverage

- How contributions affect the total benefit budget

- Whether the contribution will remain sustainable at renewal

- Whether the insurer or plan applies a minimum employer contribution

SHOP allows an eligible employer to choose how much of an employee’s dental premium the business will pay. The employer should still confirm the rules of the specific insurer, plan and state before making a final decision.

A generous contribution may encourage enrollment, but the amount should be affordable enough for the business to maintain consistently.

Employee Participation

Some small-group plans may require a minimum number or percentage of eligible employees to participate.

For SHOP health and dental coverage, businesses generally must enroll at least 70% of the employees who are offered coverage. Employees who already have qualifying coverage from another source may not count as rejecting the offer, and some states use different participation requirements. The federal SHOP participation requirement is also waived during the annual November 15–December 15 enrollment window.

Before selecting a plan, ask:

- How many eligible employees must enroll?

- How are employees with other coverage counted?

- Do state-specific participation rules apply?

- Is there a special enrollment period without a minimum participation requirement?

- What happens if participation falls below the required level at renewal?

Do not assume that every private small-group dental plan uses the same participation rules as SHOP. Confirm the requirement directly with the insurer, agent or broker.

Confirm the current participation rules for your state before selecting a plan.

Provider Network

A dental plan is more useful when employees can reasonably access participating dentists.

Review:

- The number of participating general dentists

- Access near employee homes and workplaces

- Availability of pediatric dentists

- Access to orthodontists and other specialists

- Whether employees can receive out-of-network benefits

- How often the provider directory is updated

- Whether current employee dentists participate

Do not rely only on a provider directory that may be outdated. Employees should confirm network participation with both the dental office and the plan before receiving treatment.

A network that works well for the business owner may not be convenient for employees who live in different communities.

Covered Dental Services

Review which services the plan includes and how they are categorized.

Coverage may be organized into:

- Preventive services

- Basic dental care

- Major restorative services

- Orthodontic care

- Emergency dental treatment

- Pediatric dental services

Check whether the plan may provide benefits for services such as:

- Exams and cleanings

- Dental X-rays

- Fillings

- Extractions

- Root canal treatment

- Crowns and bridges

- Dentures

- Dental implants

- Braces or clear aligners

A procedure being listed as covered does not necessarily mean the plan will pay the entire cost.

Review the applicable deductible, copayment or coinsurance, annual maximum, network rules, frequency limits and exclusions for each important service category.

Deductibles and Annual Maximums

The deductible is the amount a covered person may need to pay before certain plan benefits begin.

The annual maximum is the most the dental plan may pay toward an individual’s eligible services during a benefit year.

Small business owners should confirm:

- Whether each employee has an individual deductible

- Whether dependents have separate deductibles

- Whether a family-level deductible also applies

- Whether each covered person receives a separate annual maximum

- Which services count toward the annual maximum

- Whether preventive services are exempt from the deductible

- Whether orthodontic benefits use a separate lifetime maximum

A higher annual maximum may be useful for employees expecting major treatment, but it should be evaluated together with premiums, coverage percentages and service limitations.

Waiting Periods

Dental waiting periods can affect when benefits become available for certain services.

A plan may provide preventive benefits immediately while requiring employees to wait before becoming eligible for basic, major or orthodontic services.

Learn how dental insurance waiting periods work before choosing a plan for the business.

When comparing plans, ask:

- Which services have waiting periods?

- How long is each waiting period?

- Are waiting periods waived for employees with prior dental coverage?

- Do newly hired employees receive the same waiting periods?

- Are orthodontic waiting periods different from major-service waiting periods?

- Does changing plans restart the waiting period?

Do not confuse a dental-service waiting period with an employee eligibility waiting period.

An employee eligibility waiting period determines when a new employee may enroll in the benefit. A dental-service waiting period determines when the plan begins providing benefits for a particular category of treatment. SHOP employers may choose how long new employees must wait before enrolling, subject to applicable rules.

Enrollment and Administration

A dental benefit also creates administrative responsibilities for the business.

Before enrolling, determine who will manage:

- Employee enrollment

- Dependent enrollment

- New-hire eligibility

- Employee terminations

- Premium collection

- Employer contributions

- Employee questions

- Plan documents

- Annual renewals

- Changes in employee status

Ask the insurer, agent or broker:

- How are employees added or removed?

- Is an online enrollment system available?

- Who provides employee plan documents?

- How are billing changes handled?

- What support is available during enrollment?

- What happens when an employee leaves the business?

- When can employees change their elections?

- How are renewal rate changes communicated?

SHOP enrollment may be completed directly through an insurance company or with assistance from a SHOP-registered agent or broker. Eligible businesses can generally begin offering SHOP coverage at any time of year rather than waiting for an individual-market Open Enrollment Period.

The easiest plan to administer is not automatically the best plan, but administration should be included in the final comparison. A benefit that is difficult to explain, enroll in or maintain can create additional work for the business and confusion for employees.

⚖️PPO vs HMO Plans For Small Business Owners

Some business owners compare PPO with HMO plans.

PPO

- ✔ Greater provider flexibility

- ✔ Larger networks

- ✔ Easier specialist access

HMO

- ✔ Lower monthly costs

- ✔ Structured provider network

- ✔ Budget-conscious option

PPO and HMO structures can differ in provider flexibility, specialist access, referrals and out-of-network benefits. Review our PPO vs HMO Dental Plans guide before deciding which structure may work better for your employees.

🟢Once you’ve narrowed your options, the next step is evaluating the real costs—not just the monthly premium, but the overall value each option provides for your business.

🟢Quick cost check: Review deductibles, annual maximums, waiting periods, provider network rules and expected out-of-pocket expenses before choosing a plan.

✅Small Business Owner Dental Plan Checklist

💡Before enrolling, review:

- ✔ Monthly premium

- ✔ Annual maximum

- ✔ Waiting periods

- ✔ Provider network

- ✔ Coverage for major procedures

- ✔ Coverage for family members

- ✔ PPO or HMO structure

- ✔ Expected out-of-pocket costs

Business owners who are new to deductibles, annual maximums, PPO networks and service categories can begin with our Dental Plans guide.

❓Questions To Ask Before Enrolling

💡Before enrolling, review:

- ✔ Is my dentist in-network?

- ✔ What services are covered immediately?

- ✔ Are waiting periods required?

- ✔ What is the annual maximum?

- ✔ Does the plan cover major procedures?

- ✔ What costs should I expect to pay myself?

❓Questions To Ask Before Choosing a Plan

Before choosing a plan, consider asking:

- Which services do employees commonly ask about?

- Can employees access in-network dentists near home or work?

- How are new employees added to the plan?

- Are dependents eligible?

- What waiting periods or participation rules apply?

✅QUICK TAKEAWAYS

- ✔ Small business owners often need to evaluate dental coverage independently

- ✔ PPO and HMO plans offer different advantages

- ✔ Review provider networks carefully

- ✔ Compare total costs, not just premiums

- ✔ Waiting periods may affect certain benefits

- ✔ Family plans may simplify coverage management

💚Our Recommendation

✨Before offering dental coverage, identify exactly who needs to be covered and how much the business can contribute.

A business without eligible employees may be better served by individual or family coverage. A business with employees should compare eligibility rules, participation requirements, provider access, covered services, waiting periods, annual maximums and administrative responsibilities.

When you are ready, compare dental plans based on the needs of both the business and its employees—not only on the advertised monthly premium.

The goal is to choose a structure that employees can realistically use and that the business can manage consistently.

📚HELPFUL RESOURCES

🔥Our Editorial Standards

Dental Coverage Hub is committed to providing clear, educational and regularly reviewed information about dental plans and dental insurance.

❓Frequently Asked Questions

✅ Last reviewed: June 2026

✅ About the Author: M.D.-Content creator and researcher focused on helping consumers better understand dental plans, coverage options and dental insurance concepts.

✅ Reviewed by Dental Coverage Hub Editorial Team. Content is reviewed regularly to help ensure information remains accurate, practical and useful for consumers exploring dental coverage options in the United States.

✅ This article is intended for educational purposes only and should not be considered insurance, financial or legal advice.

Compare Dental Coverage for Your Small Business

Review plan options based on employee eligibility, provider access, covered services, waiting periods, employer contributions and total business costs.