🛡️ Dental Insurance Basics

💰 Cost and Value Guide

🇺🇸 Built for U.S. Consumers

Is Dental Insurance Worth It? Costs, Benefits, and When It Pays Off

Discover when dental insurance may provide value, who benefits most from coverage and what factors to consider before choosing a plan.

🟢What You’ll Learn

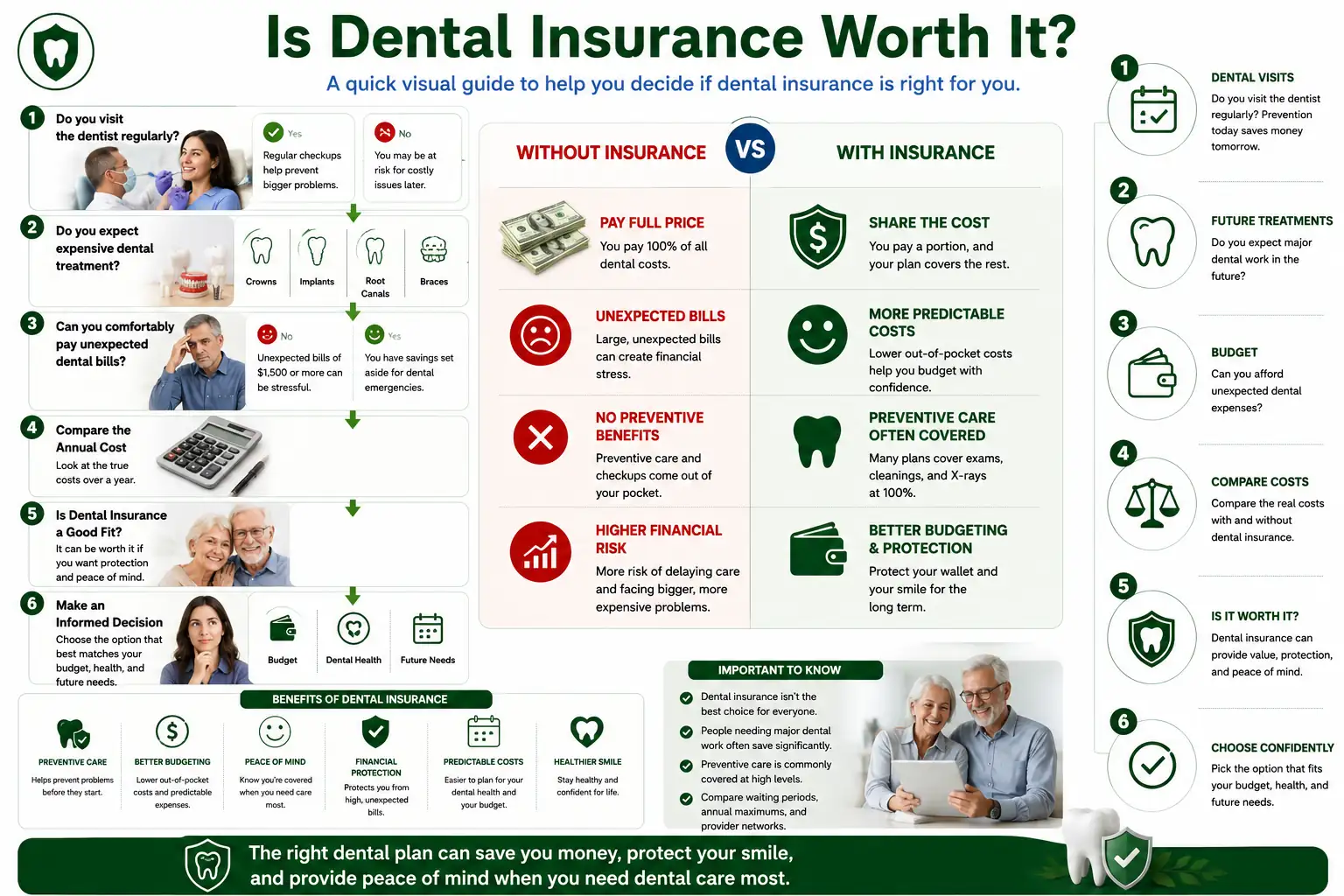

Dental insurance can be worth it, but not for everyone in the same way.

For some people, a dental plan makes routine care easier to afford and helps reduce the cost of fillings, crowns, dentures, or other covered services. For others, the premium may not make sense if the plan has a low annual maximum, long waiting periods, limited coverage, or a dentist network that does not include their preferred provider.

The real question is not simply, “Is dental insurance worth it?”

The better question is:

Will this specific dental plan give me enough value for the care I am likely to need?

This guide explains when dental insurance may be worth it, when it may not be, how it differs from health insurance, and what alternatives to consider before choosing a plan.

If you are still learning how dental insurance works, start with our Dental Plans guide to understand plan types, coverage categories, costs, provider networks and common limits before deciding whether coverage may be worth it.

Quick Answer: Is Dental Insurance Worth It?

Dental insurance may be worth it if you use preventive care, want help budgeting for dental costs, have an in-network dentist, receive employer-subsidized coverage, or expect covered dental work during the year.

It may be less valuable if the monthly premium is high, the annual maximum is low, the plan has waiting periods, your dentist is out of network, or the treatment you need is excluded.

Dental insurance is often strongest as a prevention and maintenance tool. It can help with routine exams, cleanings, X-rays, and some basic or major procedures, but it usually does not protect against large dental bills the same way major medical health insurance can.

Key Takeaways

- Dental insurance may be worth it when preventive care is covered and you actually use those benefits.

- Employer-sponsored dental insurance can be a strong value when the employer helps pay the premium.

- Individual and family dental plans can be useful, but premiums, annual maximums, waiting periods and networks matter.

- Dental insurance is not the same as health insurance. It usually helps share costs, but often has lower annual benefit limits.

- A plan may be less valuable if the care you need is excluded, delayed by a waiting period or limited by a low annual maximum.

- Dental savings plans, HSA or FSA funds, membership plans, dental schools and cash-pay options may be useful alternatives for some people.

What Does Dental Insurance Actually Do?

Dental insurance helps pay part of the cost of covered dental care.

Most plans use a mix of premiums, deductibles, copays, coinsurance, networks, annual maximums, and coverage categories. The American Dental Association explains that dental benefit plans may include deductibles, copayments, coinsurance, annual maximums, and other limitations.

In simple terms, dental insurance usually does three things:

- It encourages preventive care.

- It reduces the cost of some covered services.

- It helps make dental expenses more predictable.

But it does not usually pay for everything.

Premiums, Deductibles, Coinsurance, and Annual Maximums

A premium is the amount you pay to keep the plan active.

A deductible is the amount you may need to pay before the plan starts sharing costs for certain services.

Coinsurance means you and the plan split the cost by percentage.

A copay is a fixed amount you pay for a covered service.

An annual maximum is the most the plan will pay for covered dental care during a benefit year.

This is one of the biggest differences between dental insurance and health insurance. With many medical plans, the goal is protection from very large expenses. With many dental plans, the plan helps with routine and moderate costs but may stop paying after the annual maximum is reached.

The Common 100/80/50 Pattern

Many dental plans use a general pattern often described as 100/80/50.

That usually means preventive care may be covered at or near 100%, basic care at a lower percentage, and major care at an even lower percentage.

This is only a general pattern. Real plans vary. NADP explains that most plans cover preventive care at 100%, while basic and major services usually involve copayments or cost-sharing.

Why Dental Insurance Is Different From Health Insurance

Many people become frustrated with dental insurance because they expect it to work like health insurance.

That expectation can create confusion.

Health insurance is usually designed to protect against large, unexpected medical expenses. Dental insurance is more often designed to support prevention, maintenance, and partial cost-sharing.

That does not make dental insurance useless. It means you need to understand what it is meant to do.

Dental insurance may lower your costs, but it may not eliminate large dental bills. Crowns, dentures, implants, root canals, oral surgery, or orthodontic care may still leave you with out-of-pocket costs, especially if annual maximums, waiting periods, exclusions, or network rules apply.

How to Think About Dental Insurance Value

Dental insurance value depends on more than the monthly premium. Compare the full yearly cost, expected dental care, dentist network, annual maximum, waiting periods and covered services.

Important to Know:

- ✔ Dental insurance isn’t the best choice for everyone.

- ✔ People who need covered major dental work may get more value from a plan, depending on the plan rules.

- ✔ Preventive care is commonly covered at high levels.

- ✔ Compare waiting periods, annual maximums, and provider networks.

When Dental Insurance Is Usually Worth It

Your Employer Helps Pay the Premium

Employer-sponsored dental insurance is often one of the strongest cases for keeping dental coverage.

If your employer pays part of the premium, your actual cost may be lower than what you would pay for an individual plan. Employer plans may also have broader networks or more favorable waiting-period rules than some individual plans.

HealthCare.gov notes that small employers can offer stand-alone dental coverage and choose how much of the employee’s dental premium they pay.

You Use Preventive Care Every Year

Dental insurance may be worth it if it helps you stay consistent with exams, cleanings, and X-rays.

Preventive care can help identify cavities, gum disease, worn dental work, oral health changes, and other problems before they become more serious.

If your plan covers preventive care at a high percentage and you use those visits, you are more likely to get real value from the plan.

Learn more about what preventive dental care includes and how plans may cover routine services.

Your Dentist Is In Network

A dental plan is more valuable when your preferred dentist is in network.

In-network dentists usually agree to plan rules and negotiated fees. This can reduce your out-of-pocket costs.

If your dentist is out of network, the plan may pay less, or you may owe more than expected.

You Expect Covered Dental Work

Dental insurance may be useful if you expect covered fillings, extractions, periodontal care, crowns, dentures, or other treatment.

The key word is covered.

A plan is more valuable when the treatment you need is included, the waiting period is over, the annual maximum is enough to help, and your dentist participates in the network.

You Want More Predictable Dental Costs

Dental insurance can make costs easier to plan.

Instead of facing every bill at full price, you can review the plan’s coverage categories, network rules, copays, coinsurance, and annual maximum before treatment.

This does not remove all uncertainty, but it can give you a clearer framework.

When Dental Insurance May Not Be Worth It

You Only Need Routine Cleanings

If you only need one or two routine visits per year, the value depends on the premium and the cash price at your dental office.

Some people may pay more in premiums than they would pay directly for routine care.

That does not mean skipping dental care is wise. It only means the insurance math may not always work for very low-use patients.

The Annual Maximum Is Too Low

An annual maximum can limit how much value you receive from the plan.

If the plan stops paying after a certain amount, you may still pay a large portion of the cost for crowns, dentures, bridges, implants, or multiple procedures.

ADA materials describe annual maximums as a common benefit limitation in dental plans.

The Plan Has Long Waiting Periods

A plan may not help right away if the service you need is subject to a waiting period.

HealthCare.gov explains that if a stand-alone dental plan has a waiting period, it will not cover affected services until the waiting period ends, even though you may still pay premiums during that time.

This matters if you need a crown, root canal, denture, extraction, or other treatment soon.

Review how dental insurance waiting periods work before choosing a plan.

The Treatment You Need Is Excluded

Some dental plans exclude or limit certain services.

Implants, cosmetic dentistry, adult orthodontics, missing tooth replacement, or treatment already in progress may not be covered the way you expect.

Before buying a plan, check the exact services you may need.

Your Dentist Is Out of Network

If you want to keep your current dentist, check network participation before enrolling.

A plan may look affordable, but if your dentist does not accept it, the real value may be much lower.

How Your Situation Can Affect the Value

Dental insurance may be more or less valuable depending on how you get coverage and who needs care.

An employer plan may be a stronger value if the employer helps pay the premium. A family may compare whether multiple people will use preventive care, fillings, sealants or orthodontic evaluations. A self-employed person may compare individual dental insurance with dental savings plans or cash-pay options. An older adult may pay closer attention to dentures, periodontal care, provider networks and annual maximums.

For broader guidance based on your situation, review our Dental Insurance by Life Stage guide.

Dental Insurance Alternatives to Compare

Dental insurance is not the only way to manage dental costs. Alternatives are not always better, but they may help in certain situations.

Dental Savings Plans

A dental savings plan is not insurance. It is a discount membership program. You pay a membership fee and receive discounted rates from participating dentists. The plan does not pay the dentist for you. This may help if you need care soon, want to avoid waiting periods, or need discounts on services that insurance does not cover well.

For a deeper comparison, read our Dental Insurance vs Dental Savings Plans guide.

HSA or FSA Funds

Health Savings Accounts and Flexible Spending Accounts can help you pay for eligible dental expenses with tax-advantaged dollars. These accounts do not replace dental coverage, but they can make out-of-pocket dental costs easier to manage.

In-House Dental Membership Plans

Some dental offices offer membership plans directly to patients. These may include cleanings, exams, and discounts on other services for a set fee. The limitation is that the plan usually works only at that dental office.

Cash-Pay Discounts

Some dental offices may offer cash-pay pricing or discounts for patients without insurance. This can be useful for people who only need routine care or who prefer to avoid premiums. Always ask for a written estimate before treatment.

Dental Schools and Community Clinics

Dental schools and community clinics may provide lower-cost care. They can be helpful for people without dental insurance or for those who need a more affordable option. Availability, services, and wait times vary by location.

What to Check Before Deciding If Dental Insurance Is Worth It

- Premium. Ask how much you will pay each month and each year.

- Preventive coverage. Check whether exams, cleanings, and X-rays are covered and how often.

- Dentist network. Confirm that your preferred dentist is in network.

- Annual maximum. Check how much the plan will pay in a benefit year.

- Waiting periods. Look for waiting periods on basic, major, orthodontic, or implant-related services.

- Deductible and coinsurance. Check how much you pay before and after the plan starts sharing costs.

- Major service coverage. Review crowns, dentures, bridges, root canals, oral surgery, implants, and periodontal care.

- Exclusions. Look for cosmetic exclusions, missing tooth clauses, treatment-in-progress rules, replacement limits, and orthodontic restrictions.

For treatment-specific questions, review our Dental Insurance Coverage for Common Procedures guide.

💚Our Recommendation

Dental insurance may be worth it when it helps you use preventive care, lowers your expected dental costs, gives you access to a dentist you trust, and provides enough benefit for the services you may need.

It is often more valuable when an employer helps pay the premium, when you use preventive care regularly, or when you expect covered basic or major treatment.

It may be less valuable when the premium is high, the annual maximum is low, your dentist is out of network, or the treatment you need is excluded or delayed by a waiting period.

Do not judge a dental plan only by the monthly premium.

Compare the full picture: preventive coverage, network access, annual maximums, waiting periods, deductibles, coinsurance, exclusions, and alternatives.

The best choice is not always “insurance” or “no insurance.” It is the option that gives you the clearest value for your mouth, your budget, and your expected care.

When you are ready to review options, compare dental plans by looking at premiums, preventive coverage, dentist networks, annual maximums, waiting periods, exclusions and the care you expect to need.

Helpful Resources

- Dental Plans Guide

- Preventive Dental Care

- How Dental Insurance Waiting Periods Work

- No Waiting Period Dental Insurance

- Dental Insurance vs Dental Savings Plans

- PPO vs HMO Dental Plans

- Dental Insurance Coverage for Common Procedures

- Dental Insurance by Life Stage

- Compare Dental Plans

- Dental Insurance Learning Center

Sources

- American Dental Association — Introduction to Dental Benefits

- American Dental Association — Typical Dental Plan Benefits and Limitations

- HealthCare.gov — Dental Coverage in the Marketplace

- HealthCare.gov — Dental Coverage Glossary

- HealthCare.gov — SHOP Dental Coverage

- National Association of Dental Plans — Dental Benefits 101

🔥Our Editorial Standards

Dental Coverage Hub is committed to providing clear, educational and regularly reviewed information about dental plans and dental insurance.

Frequently Asked Questions

Is dental insurance worth it?

Dental insurance can be worth it if you use preventive care, have an in-network dentist, receive employer-subsidized coverage, or expect covered dental work.

It may not be worth it if the premium is high, the annual maximum is low, your dentist is out of network, or the treatment you need is excluded.

Is dental insurance worth it if I only need cleanings?

It depends on the premium, the cost of cleanings in your area, and whether preventive care is covered.

If you only need routine care, compare the yearly premium against the cash price of those visits.

Is employer dental insurance worth it?

Employer dental insurance is often worth considering because the employer may help pay the premium.

However, you should still check the network, annual maximum, waiting periods, and coverage for the services you may need.

What is better: dental insurance or a dental savings plan?

Neither is automatically better.

Dental insurance may be better if you want covered preventive care and help with eligible services. A dental savings plan may be better if you want immediate discounts, no insurance claims, and a participating dentist offers useful reduced rates.

What should I compare before choosing dental insurance?

Compare premiums, preventive coverage, dentist networks, deductibles, coinsurance, annual maximums, waiting periods, major service coverage, exclusions, and alternatives such as dental savings plans.

Why does dental insurance have annual maximums?

Dental insurance plans often use annual maximums to limit how much the plan will pay toward covered dental care during a benefit year.

This is one reason dental insurance works differently from major medical health insurance. A dental plan may help with preventive care and share part of the cost for basic or major services, but once the annual maximum is reached, the member may be responsible for additional costs for the rest of that benefit year.

Before choosing a plan, compare the annual maximum with the premium, expected dental needs, coinsurance, waiting periods and covered services.

Does dental insurance help with major dental work?

Dental insurance may help with major dental work if the service is covered by the plan and the plan rules have been met.

Major services may include crowns, bridges, dentures, root canals, oral surgery or some periodontal procedures, depending on how the plan classifies care. However, major dental work is often subject to coinsurance, deductibles, annual maximums, waiting periods, replacement limits and exclusions.

A plan may reduce part of the cost, but it may not pay the full amount. Always check the exact procedure, service category, waiting period and annual maximum before scheduling treatment.

When may dental insurance not be worth it?

Dental insurance may be less valuable if the monthly premium is high, the annual maximum is low, your preferred dentist is out of network, or the care you need is excluded or delayed by a waiting period.

It may also be less useful if you only need routine cleanings and the yearly premium costs more than paying directly for preventive visits. In that case, it may still be important to keep up with dental care, but the insurance math may not work as well.

The best way to decide is to compare the total yearly cost, including premiums, deductibles, coinsurance, annual maximums, network rules and the dental care you expect to need.

Last reviewed: July 12, 2026

Author Note ;Reviewed by Dental Coverage Hub Editorial Team

Content is reviewed regularly to help ensure information remains accurate, practical and useful for consumers exploring dental coverage options in the United States.

✅ This article is intended for educational purposes only and should not be considered insurance, financial or legal advice.

Ready to Compare Dental Plans?

Compare dental plans by cost, coverage, waiting periods and dentist access before deciding what fits your needs.