Dental Insurance vs Dental Savings Plans: What’s the Difference?

🇺🇸 Built for U.S. Consumers

💰Understand Costs

🦷 Compare Both Options

🟢What You’ll Learn

Dental care can get expensive quickly, especially if you need more than a routine cleaning. A filling, crown, denture, root canal, implant, or braces can create a bill that makes many people start searching for ways to lower the cost.

Two common options are dental insurance and dental savings plans. They may sound similar, but they work very differently.

Dental insurance helps pay part of the cost of eligible dental care. A dental savings plan, also called a dental discount plan, does not pay part of your bill. Instead, it gives you access to discounted rates from participating dentists.

The better choice depends on your dental needs, your budget, your dentist, your timing, and whether you want coverage, discounts, or both.

This guide explains how dental insurance and dental savings plans work, how their costs differ, and which option may make more sense in common real-life situations.

If you are still learning how dental plans work, start with our Dental Plans guide to understand plan types, costs, coverage categories, waiting periods and common limits.

Quick Answer

Dental insurance is coverage. You pay premiums, and the plan may help pay for preventive, basic, and major dental services according to the plan’s rules.

A dental savings plan is not insurance. It is a membership program that gives you access to discounted prices from participating dentists. You pay the discounted fee directly to the dentist.

Dental insurance may be a better fit if you want help paying for covered care, preventive services included at or near 100%, and predictable coverage rules. A dental savings plan may be a better fit if you want immediate discounts, no waiting periods, no annual maximum, or savings on services that insurance may limit or exclude.

Neither option is automatically better. The right choice depends on the dental work you expect to need and how each plan handles your specific dentist, procedure, and costs.

Key Takeaways

Dental insurance and dental savings plans are not the same thing. Insurance may pay part of eligible dental costs. A savings plan only gives you access to discounted rates.

Dental insurance can help with covered preventive, basic, and major care, but it may include premiums, deductibles, coinsurance, waiting periods, exclusions, and annual maximums. HealthCare.gov notes that stand-alone dental plans with waiting periods do not cover affected services until the waiting period ends.

Dental savings plans usually have no claims, no deductibles, no waiting periods, and no insurance annual maximums. However, you must use participating dentists and pay the discounted cost yourself.

Savings plans can be useful for immediate care, cosmetic services, or costs above an insurance annual maximum. They do not remove the need to pay the dental office.

Dental insurance can be more valuable when preventive care is covered, an employer pays part of the premium, or your expected treatment fits well within the plan’s coverage limits.

The best choice is based on the math. Compare the yearly premium or membership fee, dentist participation, expected procedures, waiting periods, coverage percentages, annual maximums, and discounted fee schedule before enrolling.

What Is Dental Insurance?

Dental insurance is a type of dental benefit plan that may help pay part of the cost of covered dental care.

You usually pay a monthly premium to keep the plan active. When you visit a dentist, the plan may pay part of the approved cost for eligible services. Your share may depend on the deductible, copay, coinsurance, annual maximum, dentist network, and plan exclusions.

Many dental insurance plans divide services into categories such as preventive, basic, and major care. Preventive care often includes exams, cleanings, and X-rays. Basic care may include fillings and simple extractions. Major care may include crowns, bridges, dentures, root canals, oral surgery, or other more expensive treatment, depending on the plan.

The American Dental Association explains that dental benefit plans often use cost-sharing tools such as deductibles, copayments, coinsurance, limitations, and annual maximums.

How Dental Insurance Pays for Care

Dental insurance usually pays according to the plan’s benefit structure.

A common example is the 100/80/50 model. Under this type of structure, preventive care may be covered at or near 100%, basic services at around 80%, and major services at around 50%.

This is only a general example. Real plan details vary by insurer, state, employer, network, and policy.

For example, one plan may cover a filling at 80% after the deductible. Another may cover the same filling at a different percentage. A third plan may require a waiting period before basic care is covered.

Common Dental Insurance Costs

A premium is the amount you pay monthly to keep the plan active.

A deductible is the amount you may need to pay before the plan starts paying for certain covered services.

Coinsurance is the percentage split between you and the plan. If a plan pays 50% for major care, you may pay the other 50%, plus any deductible or noncovered charges.

A copay is a fixed amount you pay for a covered service.

An annual maximum is the most the plan will pay for covered dental services during a benefit year. Once the plan reaches that limit, you usually pay the remaining costs yourself.

Dental Insurance Limitations to Watch For

Dental insurance can be helpful, but it is not unlimited coverage.

A plan may have waiting periods for basic or major services. It may also have exclusions for certain procedures, such as cosmetic treatments or implants. Some plans limit how often they pay for crowns, dentures, X-rays, or periodontal treatment.

The annual maximum is especially important. If your plan has a $1,500 annual maximum and you need several expensive procedures in the same year, the plan may stop paying before your treatment is complete.

What Is a Dental Savings Plan?

A dental savings plan, also called a dental discount plan, is a membership program that provides access to reduced fees from participating dentists.

It is not dental insurance.

Cigna describes discount dental programs as annual, fee-based membership programs that offer discounts on dental services and are not dental insurance. Delta Dental also explains that a dental discount plan is not insurance, but a program that provides savings through a network of dentists who agree to charge less.

How Dental Savings Plans Work

With a dental savings plan, you pay a membership fee. This may be annual or monthly, depending on the program.

After activation, you use a participating dentist and pay the discounted rate directly to the dental office.

There are usually no insurance claims. The plan does not reimburse you. It does not pay the dentist on your behalf. It simply gives you access to a reduced fee schedule or discount.

MetLife explains that dental discount plans are not insurance and that members pay the dentist directly at a discounted rate.

What Dental Savings Plans Usually Do Not Have

Dental savings plans usually do not have insurance deductibles.

They usually do not have insurance waiting periods.

They usually do not have insurance annual maximums.

They usually do not require claims processing.

However, this does not mean dental care is free. You still pay the dentist. The savings plan only reduces the price if the dentist participates and the service is eligible for a discount.

Dental Savings Plan Limitations to Watch For

A dental savings plan is only useful if your dentist accepts it or if you are willing to use a participating dentist.

Discounts can vary by plan, ZIP code, provider, and procedure. Aetna states that fee schedules and savings may vary by ZIP code and provider, and that the savings plans are not dental insurance.

Some services may receive a smaller discount than others. Specialist care, cosmetic procedures, implants, orthodontics, and complex treatment may follow different discount rules.

You should always check the fee schedule before enrolling.

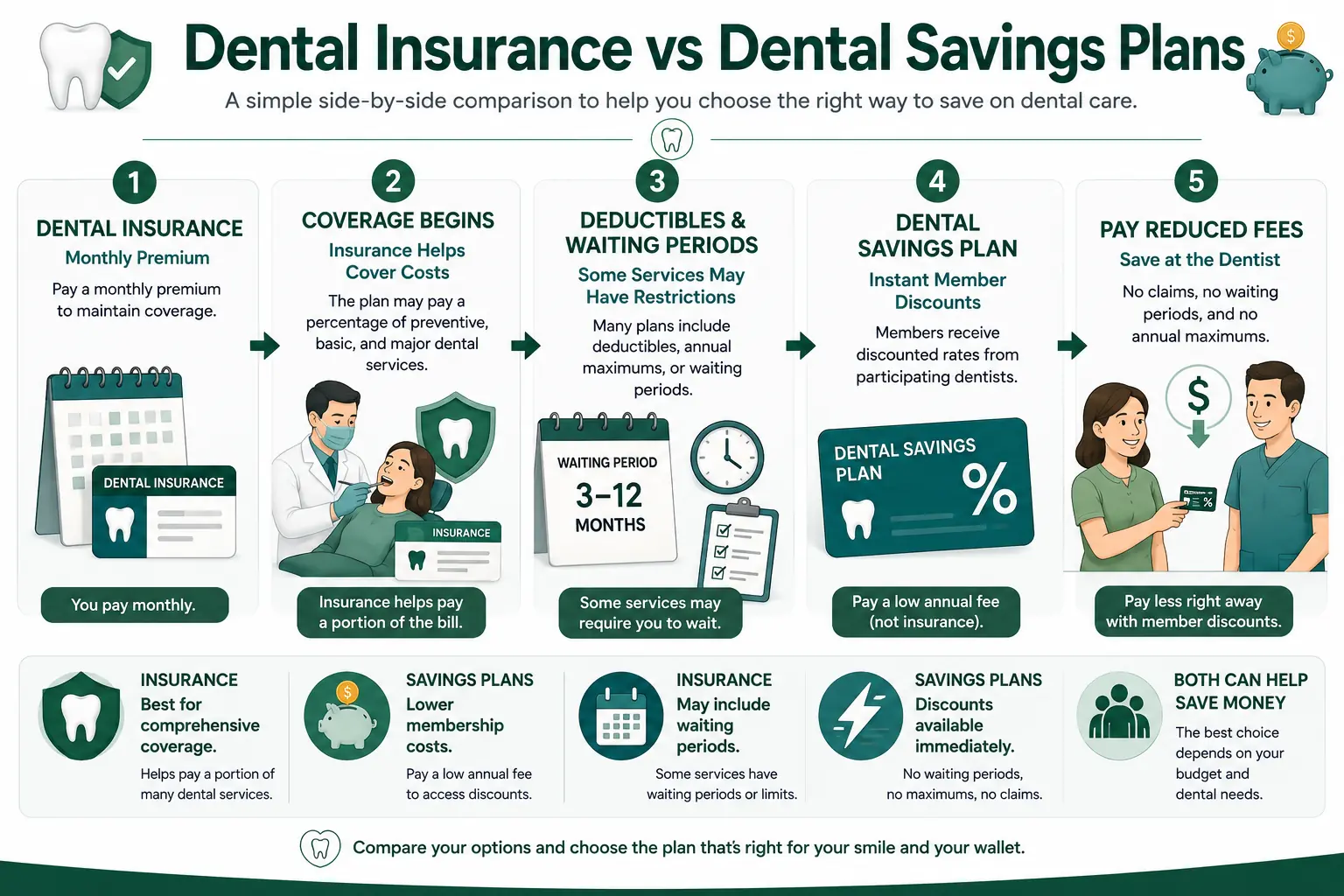

Visual Overview: Dental Insurance vs Dental Savings Plans

A simple side-by-side comparison to help you choose the right way to save on dental care.

Dental insurance usually works through premiums, covered benefits and plan rules. Dental savings plans usually work through membership fees and discounted rates from participating dentists.

Dental Insurance vs Dental Savings Plans: Main Differences

| Feature | Dental Insurance | Dental Savings Plan |

|---|---|---|

| Monthly premium | Usually yes | Usually no |

| Membership fee | Usually no | Usually yes |

| Claims process | Usually yes | No insurance claims |

| Provider network | Often required for lower costs | Required for discounts |

| Waiting periods | May apply | Usually no insurance-style waiting period |

| Annual maximums | Common | Usually no insurance annual maximum |

| Discounts | Based on covered benefits | Based on negotiated discounts |

| Best fit | People who want insurance-style coverage | People who want membership-based discounts |

Which Option Costs Less?

The answer depends on what dental care you expect to need.

Dental insurance and dental savings plans are priced differently. Insurance usually has monthly premiums and may pay part of covered care. A savings plan usually has a membership fee and reduces the price of services.

That means you should compare:

- Annual premiums or membership fees

- Deductibles

- Coinsurance or copays

- Discounted fee schedules

- Annual maximums

- Waiting periods

- Dentist participation

- Expected procedures

The only fair comparison is the total expected yearly cost: premiums or membership fees, dentist participation, expected procedures, waiting periods, annual maximums and any discounted fee schedule.

When Dental Insurance May Make More Sense

Dental insurance may be a better fit when you want a structured coverage plan and your expected care is included under the policy.

Employer-Subsidized Premiums

If your employer pays part of your dental insurance premium, insurance may become much more valuable.

For example, an employer-sponsored plan may cost less for the employee if the employer contributes toward the premium.

In that case, dental insurance may beat a savings plan even for routine care.

Preventive Care Covered at or Near 100%

Dental insurance can be useful for people who want help staying consistent with cleanings, exams, and X-rays.

Many dental insurance plans cover preventive care at a high percentage when you use an in-network dentist. This can make regular visits easier to budget for.

Covered Basic and Major Care

Dental insurance may help if you expect fillings, extractions, root canals, crowns, dentures, or periodontal treatment and those services are covered.

The key is to check the waiting period, deductible, coinsurance, annual maximum, and dentist network.

Better Network Pricing

A dental insurance plan may have negotiated in-network rates that reduce the approved cost before coinsurance is applied.

This can make the final cost lower than expected, especially when the dentist participates in the plan’s network.

When a Dental Savings Plan May Make More Sense

A dental savings plan may be a better fit when you want discounts without traditional insurance rules.

You Need Care Right Away

Dental savings plans often activate quickly and usually do not have insurance-style waiting periods.

This can be helpful if you need a crown, extraction, denture, root canal, or other treatment soon and dental insurance would require you to wait.

You Want No Annual Maximum

Dental savings plans generally do not have an insurance annual maximum.

This means the discount may apply to eligible services throughout the year, as long as you use participating providers and follow the plan’s rules.

This can matter when you need multiple procedures in the same year.

You Need a Service Insurance May Exclude

Dental insurance may exclude or limit cosmetic services, implants, adult orthodontics, or treatment that began before the policy became active.

A dental savings plan may offer discounts on some of these services, depending on the participating provider and fee schedule.

You Prefer Simpler Payment

Dental savings plans usually do not involve claims.

You pay the dentist directly at the discounted rate. This can feel simpler than waiting for a claim to process.

Can You Use Dental Insurance and a Dental Savings Plan Together?

Sometimes, yes, but not always in the way people expect.

You generally should not assume that you can stack insurance benefits and a savings plan discount on the same procedure. Many dental offices will require you to use one payment arrangement for a given service.

However, some people keep both types of plans.

For example, dental insurance may be used for preventive care and covered services. A savings plan may help with services not covered by insurance, cosmetic treatment, or costs after the insurance annual maximum has been reached.

Before enrolling in both, ask the dental office these questions:

- Can I use this dental savings plan at your office?

- Can I use it for services my insurance does not cover?

- Can I use it after my insurance annual maximum is reached?

- Can I use it for cosmetic services or implants?

- Can I switch between insurance and the savings plan for different procedures?

The answer depends on the dental office, the insurance contract, the savings plan, and the procedure.

How to Choose Between Dental Insurance and a Dental Savings Plan

Step 1: Start With the Dental Care You Expect to Need

Do not choose based only on the name of the product.

Start with your actual needs.

- Are you only planning cleanings and exams?

- Do you need fillings?

- Are you expecting a crown, denture, implant, or root canal?

- Does your child need braces?

- Are you a senior comparing denture, crown, or implant costs?

The answer changes the math.

Step 2: Ask Your Dentist for Procedure Codes and Fees

If you already know you need treatment, ask your dentist for a written treatment plan.

It should include procedure codes, estimated fees, and timing.

This helps you compare insurance benefits and savings plan discounts more accurately.

Step 3: Check Dentist Participation

A plan is only useful if you can use it with the dentist you want.

For dental insurance, confirm whether the dentist is in network.

For a dental savings plan, confirm whether the dentist participates in that specific discount program.

Do not rely only on online directories. Call the dental office directly.

Step 4: Compare the Total Yearly Cost

For dental insurance, add:

- Annual premiums

- Deductible

- Coinsurance or copays

- Costs above the annual maximum

- Noncovered services

- Out-of-network charges

For a dental savings plan, add:

- Membership fee

- Discounted dental fees

- Any services not discounted

The total yearly cost matters more than the monthly price.

Step 5: Review Waiting Periods

Dental insurance may have waiting periods for basic or major services.

HealthCare.gov advises consumers to get details from the insurance company about waiting periods before enrolling in a stand-alone dental plan.

Dental savings plans usually do not have insurance-style waiting periods, but you should still confirm the activation date.

Step 6: Check Annual Maximums

If you expect major dental work, the annual maximum is one of the most important numbers in the insurance plan.

A plan that pays 50% for major services may still provide limited value if the annual maximum is low and the treatment cost is high.

Dental savings plans generally do not use an insurance annual maximum, but the discount percentage may be smaller for certain services.

Step 7: Read Exclusions Carefully

Both options have limitations.

Dental insurance may exclude cosmetic treatment, implants, adult orthodontics, replacement of missing teeth, or treatment already in progress.

Dental savings plans may exclude certain services from discounts or may offer reduced savings for specialists.

Always read the official plan details before enrolling.

How Your Situation Can Affect the Choice

Your situation can affect which option is easier to use. A family, a retiree, a self-employed person or an employee choosing workplace benefits may compare different priorities.

For broader guidance by situation, review our Dental Insurance by Life Stage guide.

💚Our Recommendation

Do not choose dental insurance or a dental savings plan based only on which one sounds cheaper.

Choose dental insurance if you want structured coverage, preventive benefits, possible help with covered basic and major care, and especially if an employer helps pay the premium.

Choose a dental savings plan if you want immediate discounts, no insurance annual maximum, no claims process, and possible savings on services insurance may limit or exclude.

If you expect only routine cleanings, compare the annual premium against the actual cash price and the savings plan fee.

If you expect a filling, crown, denture, implant, or braces, ask your dentist for procedure codes and compare the real numbers.

The best option is the one that lowers your total cost with a dentist you are willing to use, for the treatment you are likely to need.

When you are ready to review options, compare dental plans based on costs, provider access, waiting periods and expected dental needs.

Questions to Ask Before You Enroll

| Question | Why it matters |

|---|---|

| Is this insurance or a discount membership? | The two products work differently. |

| Does my dentist participate? | Savings and benefits depend on provider participation. |

| What is the annual premium or membership fee? | Fixed costs affect the real yearly value. |

| Are there waiting periods? | Dental insurance may delay benefits for some services. |

| Is there an annual maximum? | Insurance may stop paying after the plan limit. |

| What services are covered or discounted? | Benefits and discounts vary by plan and procedure. |

| What will I pay at the dental office? | Savings plans usually require direct payment. |

| Can I use this with existing insurance? | Some offices allow separate use; others do not. |

| Can I see the fee schedule before enrolling? | The discount is useful only if the final price makes sense. |

📚Helpful Resources

🔥Our Editorial Standards

Dental Coverage Hub is committed to providing clear, educational and regularly reviewed information about dental plans and dental insurance.

Sources

- HealthCare.gov — Dental Coverage in the Marketplace.

- American Dental Association — An Introduction to Dental Benefits.

- Cigna Healthcare — Discount Dental Programs.

- Delta Dental — What Is a Dental Discount Plan?

- MetLife — What Is a Dental Discount Plan?

- Aetna Dental Offers — Aetna Vital Savings.

- DentalPlans.com — How It Works.

Frequently Asked Questions

What is the difference between dental insurance and a dental savings plan?

Dental insurance may pay part of the cost of covered dental care after premiums, deductibles, copays, coinsurance, and plan rules are applied.

A dental savings plan is not insurance. It gives you access to discounted rates from participating dentists, and you pay the discounted price directly.

Is a dental savings plan the same as dental insurance?

No. A dental savings plan is a membership discount program, not insurance.

It does not pay claims, reimburse you, or cover a percentage of the bill the way insurance may. It simply reduces the price if you use a participating dentist.

Are dental savings plans worth it?

A dental savings plan may be worth it if the discount you receive is greater than the membership fee and if your dentist participates.

It may be especially useful for immediate care, cosmetic services, or dental work that insurance does not cover well.

Is dental insurance better than a dental savings plan?

Dental insurance may be better if preventive care is covered, your employer pays part of the premium, and your expected treatment is covered within the annual maximum.

A dental savings plan may be better if you need care quickly, want no waiting period, or need discounts on services that insurance may exclude.

Do dental savings plans have waiting periods?

Dental savings plans usually do not have insurance-style waiting periods.

However, you should confirm when the membership becomes active and when you can begin using the discount.

Do dental savings plans have annual maximums?

Dental savings plans usually do not have insurance annual maximums.

You can generally use the discount for eligible services throughout the membership period, as long as you use participating providers.

Does dental insurance have an annual maximum?

Many dental insurance plans have an annual maximum.

This is the most the plan will pay for covered dental care during a benefit year. After the plan reaches that amount, you usually pay additional costs yourself.

Can I use dental insurance and a dental savings plan together?

Sometimes, but you usually cannot assume they can be combined on the same procedure.

Some people use insurance for covered services and a savings plan for services not covered by insurance or after reaching the annual maximum. Always ask the dental office before treatment begins.

Last reviewed: July 10, 2026

About the Author: M.D.-Content creator and researcher focused on helping consumers better understand dental plans, coverage options and dental insurance concepts.

Reviewed by Dental Coverage Hub Editorial Team. Content is reviewed regularly to help ensure information remains accurate, practical and useful for consumers exploring dental coverage options in the United States.

✅ This article is intended for educational purposes only and should not be considered insurance, financial or legal advice.

Compare Dental Plans With Confidence

Dental insurance and dental savings plans work differently. Compare costs, dentist access, waiting periods and plan limits before choosing an option.