📚 Educational Resources

🇺🇸 Built for U.S. Consumers

📋 Compare Plans Easily

No Waiting Period Dental Insurance: 2026 Guide

Need Dental Coverage Quickly? Here’s What to Know About No Waiting Period Plans

🟢What You’ll Learn

You may already know that you need a filling, extraction, root canal, crown, or denture. The problem is that many individual dental insurance plans make new members wait several months before benefits become available for basic or major dental work.

Dental insurance with no waiting period may help you use certain benefits sooner. However, the phrase “no waiting period” can mean different things from one plan to another. One policy may cover only exams and cleanings immediately, while another may make fillings, crowns, root canals, or dentures eligible as soon as the policy becomes effective.

Even when a procedure is immediately eligible, the plan may pay only a small percentage during the first year. You may also have to meet a deductible, stay within an annual maximum, use an in-network dentist, or follow other plan limitations.

This guide explains how no-waiting-period dental insurance works, which services may be available sooner, what you could still pay out of pocket, and what to check before enrolling.

If you are still learning how dental waiting periods work, start with our How Dental Insurance Waiting Periods Work guide before comparing no-waiting-period plan options.

Quick Answer: What Is No Waiting Period Dental Insurance?

Dental insurance with no waiting period allows you to use covered benefits as soon as your policy becomes effective, rather than waiting three, six, or twelve months.

That does not necessarily mean every dental procedure is covered immediately or in full. A plan may have no waiting period but still pay only 20% of a crown during the first year. Another may provide immediate access to major services but limit you to a specific network or primary dentist.

Before enrolling, confirm the policy effective date, whether your exact procedure is covered, the first-year coverage percentage, deductible, annual maximum, network rules, frequency limitations, and exclusions.

HealthCare.gov warns that stand-alone dental plans may require adults to pay premiums during a waiting period even though affected services are not yet covered. It recommends checking the waiting-period rules directly with the insurer before enrolling.

Key Takeaways

- No waiting period does not always mean full coverage.

- Preventive care is the most likely category to be available immediately.

- Basic, major, orthodontic and implant-related services may follow different rules.

- First-year benefits matter because some plans use graded benefits.

- Dentist network rules can change your final cost.

- Always verify the official plan documents before enrolling.

What Is Dental Insurance With No Waiting Period?

A dental insurance waiting period is the length of time you must remain enrolled before the plan begins paying for a particular category of care.

A plan might provide immediate preventive benefits but require a six-month wait for fillings and a twelve-month wait for crowns, dentures, or other major services. Other policies eliminate waiting periods for all covered categories.

A no-waiting-period plan removes this time-based restriction. Once the policy becomes effective, eligible services can be considered for benefits under the plan.

However, a service can be covered by the policy without being fully payable. According to the American Dental Association, payment may still be reduced or prevented by deductibles, annual maximums, frequency limits, waiting periods, and other contractual limitations.

This distinction is especially important when you already need treatment.

A crown may be eligible immediately, for example, but the plan could pay only 20% during the first year. If the crown has an approved network cost of $1,200, immediate eligibility may still leave you responsible for most of the bill.

How No Waiting Period Dental Insurance Works

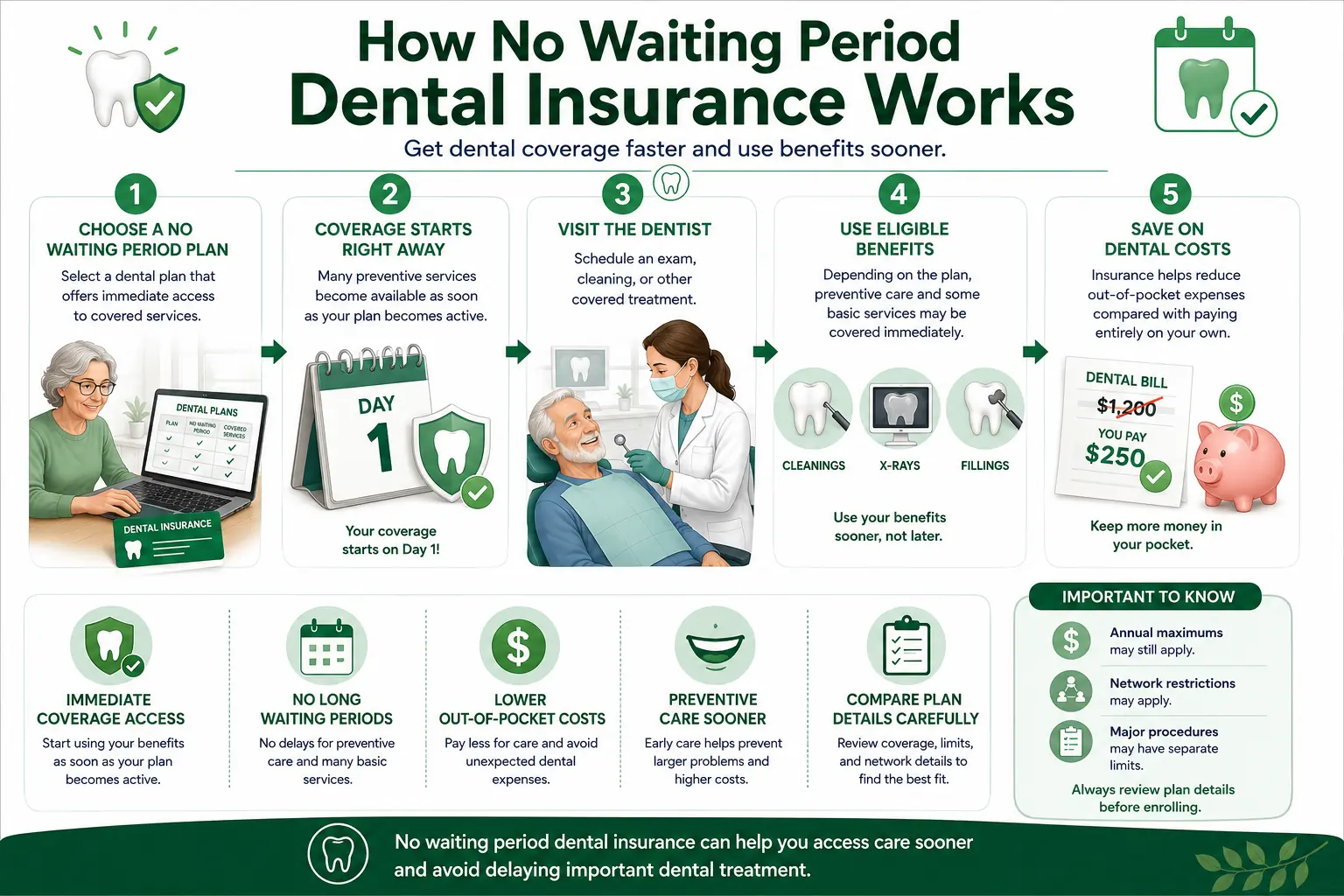

This visual overview shows how no-waiting-period dental insurance may allow eligible benefits to begin sooner, while deductibles, annual maximums, network rules and procedure limits may still apply.

Does No-Wait Coverage Really Begin Immediately?

The answer depends on what the plan means by “immediate.”

Enrollment Date

This is the date on which you complete your application and submit any required payment.

Policy Effective Date

This is the date on which your insurance coverage officially begins. It may not be the same day that you submit the application.

A plan with no waiting period generally allows covered benefits to begin on the effective date. It does not necessarily provide retroactive coverage for care received before that date.

Treatment Eligibility

Your procedure must be included as a covered service. A policy can have no waiting period but still exclude implants, cosmetic procedures, certain types of dentures, or treatment that began before enrollment.

Benefit Payment

The plan applies its deductible, coinsurance, copayment, annual maximum, network allowance, and other limitations before determining how much it will pay.

Therefore, “no waiting period” should be understood as:

You do not have to complete an additional time-based waiting period after the policy becomes effective before an eligible service can be considered for benefits.

It should not be understood as:

Every treatment will be free, fully covered, approved, or available on the day you apply.

What Dental Services May Be Covered Without a Waiting Period?

Dental plans usually organize care into preventive, basic, and major service categories. The classification of a procedure can vary by policy, so always verify how your plan categorizes the treatment you need.

| Type of dental care | Common examples | How no-wait coverage may work | What to verify |

|---|---|---|---|

| Preventive care | Exams, cleanings, routine X-rays | Often available as soon as the policy becomes effective | Frequency limits, network rules and effective date |

| Basic care | Fillings, simple extractions, basic periodontal care | May be available sooner under some no-wait plans | Deductible, coinsurance, copays and service category |

| Major care | Crowns, bridges, dentures, root canals | May have no waiting period, but first-year benefits may be limited | Annual maximum, coverage percentage and replacement limits |

| Orthodontic care | Braces, clear aligners, retainers | May have separate rules or may not be included | Age limits, lifetime maximums and orthodontic exclusions |

| Dental implants | Implant placement, abutment, implant crown | May be covered, limited or excluded depending on the plan | Implant-specific rules, missing tooth clauses and benefit limits |

These are general patterns only. A plan may advertise no waiting period for one category of care while limiting or excluding another. Always confirm the exact procedure code, service category, first-year benefit level and provider network before enrolling.

For treatment-specific questions, review our Dental Insurance Coverage for Common Procedures guide.

No Waiting Period Does Not Mean No Out-of-Pocket Costs

Several plan features can affect what you pay even when the procedure is eligible immediately.

Deductible

The deductible is the amount you must pay toward eligible services before the plan begins contributing.

Some policies use an annual deductible that resets every year. Others use a one-time or lifetime deductible that does not reset while you remain continuously enrolled.

Coinsurance

Coinsurance is the percentage of the approved cost paid by the plan and the member.

When a plan says that major services are covered at 20%, the insurer generally pays 20% of the eligible amount after applicable deductibles. You are responsible for the remaining amount and possibly any noncovered charges.

Copayment

DHMO or copay plans often use a fixed schedule. Instead of paying a percentage, you pay a stated amount for each covered procedure when you use the required network provider.

This can make costs more predictable, but access to dentists and specialists may be more restricted.

Annual Maximum

The annual maximum is the most the insurance plan will pay during a benefit year for covered services subject to that maximum.

Once it is exhausted, you generally become responsible for additional treatment costs, even though the procedures remain covered services under the policy. The ADA notes that annual maximums of $1,000 or $1,500 remain common, although higher maximums are also available.

Network Allowance

An in-network dentist has agreed to accept negotiated fees for covered services. This can lower the amount on which your deductible and coinsurance are calculated.

When you use an out-of-network dentist, the insurer may calculate its payment using a different allowed amount. You may then owe your coinsurance plus the difference between the plan allowance and the dentist’s actual fee.

Graded Benefits

Graded benefits increase over time. A plan may provide immediate eligibility while paying a lower percentage or offering a lower annual maximum during the first year.

This structure is common among no-waiting-period policies designed to discourage someone from enrolling only when expensive treatment is already needed.

How to Compare No-Waiting-Period Dental Plans

When comparing no-waiting-period dental plans, do not focus only on the headline. Compare:

- Which service categories have no waiting period

- The policy effective date

- First-year coverage percentages

- Deductibles and copays

- Annual maximums

- Dentist network rules

- Exclusions

- Treatment already started before enrollment

- Missing tooth clauses

- Whether the plan uses graded benefits

A plan with no waiting period may still provide limited first-year value if the covered percentage is low or the annual maximum is small.

Important Limitations to Check Before Enrolling

Low First-Year Coverage

A plan can truthfully advertise no waiting period while paying only 10%, 20%, or 30% for certain first-year services.

Compare the actual dollar benefit with the premiums and deductible you expect to pay.

Treatment Started Before the Effective Date

Work that began before coverage became effective may be excluded.

For a crown, denture, implant, bridge, root canal, or orthodontic treatment, ask the insurer what event it considers the treatment start date. It may be the preparation date, extraction date, impression date, appliance placement date, or another stage defined by the policy.

Missing Tooth Clause

A missing tooth clause may restrict benefits for replacing a tooth that was already absent before the policy started.

Ask specifically whether a bridge, partial denture, full denture, or implant replacing an existing missing tooth will be covered.

Frequency Limitations

Plans may limit how often they pay for cleanings, X-rays, crowns, dentures, periodontal treatment, or replacement appliances.

A covered crown may still receive no payment if the tooth had another crown within the policy’s replacement period.

Alternate Benefit Provisions

A plan may approve a less expensive treatment instead of the treatment selected by you and your dentist.

For example, the policy might base its payment on a metal crown even if you choose a more expensive material. You may be responsible for the difference.

Annual Maximums

A high coverage percentage can be less valuable when the annual maximum is low.

If a policy pays 50% for major services but has only $1,000 available for the entire year, several procedures can exhaust the benefit quickly.

Network Restrictions

A PPO may allow out-of-network care but pay less or expose you to balance billing.

A DHMO may provide no out-of-network benefits except in limited emergencies. You may need to use a designated primary care dentist and obtain referrals for specialists.

Preauthorization and Predetermination

“No waiting period” does not remove all administrative requirements.

For expensive treatment, ask your dentist to submit a predetermination or pre-treatment estimate. This is not always a payment guarantee, but it can show how the insurer expects to process the proposed services.

For expensive treatment, ask your dental office whether a predetermination or pre-treatment estimate can be submitted before care begins.

How to Compare Plans When You Need Treatment Soon

Start With the Treatment, Not the Company Name

Ask your dentist for a written treatment plan that includes the procedure names, CDT codes, estimated fees and expected treatment dates.

Searching for a general “full coverage” plan is less useful than determining whether the exact procedure code is covered.

Confirm the Effective Date

Ask the insurer:

“When will my policy become effective if I enroll and pay today?”

Do not schedule treatment based only on the application date.

Verify the Waiting Period by Procedure

Ask:

“Is there a waiting period for this exact procedure code?”

Do not accept a general statement that the plan has “immediate benefits” unless the representative confirms the category and procedure.

Check the First-Year Percentage

Ask how much the plan pays in the first benefit year, not only the maximum percentage advertised for later years.

A plan that eventually pays 50% may pay only 20% during the first year.

Ask for the Deductible and Annual Maximum

Determine whether the deductible is annual or one-time and whether preventive services are exempt.

Confirm the year-one annual maximum and whether preventive services reduce the amount available for restorative treatment.

Confirm the Network

Use the insurer’s directory and call the dental office directly.

Ask whether the dentist currently participates in the exact network associated with the plan. A dentist may accept plans from the same company but not participate in every network or product.

Check Existing Treatment and Missing Tooth Rules

Tell the insurer whether the tooth is already missing, whether treatment was recommended, and whether any part of the procedure has begun.

Ask for the answer in writing or locate the relevant provision in the certificate of coverage.

Compare the Total First-Year Cost

Estimate:

Annual premiums + deductible + expected coinsurance or copayments + noncovered charges.

Then subtract the amount the plan is expected to pay.

Compare that result with negotiated cash fees, a dental discount plan, an office membership plan, or financing offered by the dentist.

Can a Dental Insurance Waiting Period Be Waived?

Sometimes, yes. Some plans may waive or reduce waiting periods if you had recent comparable dental coverage before enrolling.

The rules vary by insurer and plan. You may need to show proof of prior coverage and avoid a gap between policies.

Do not assume a waiver applies automatically. Ask the insurer what documentation is required and get the answer in writing before starting treatment.

Dental Insurance vs a Dental Discount Plan

A dental discount plan is not insurance. It usually provides access to reduced fees from participating dentists, and the member pays the discounted charge directly to the dental office.

A discount plan may be worth comparing if you need care soon and insurance benefits are delayed, limited or excluded. However, it does not pay a percentage of your bill like insurance.

For a deeper comparison, read our Dental Insurance vs Dental Savings Plans guide.

What to Do If You Need Dental Treatment Right Away

Get a Diagnosis Before Choosing a Plan

Dental pain does not reveal the exact procedure you need. What appears to be a filling could require a root canal and crown, while a painful tooth could need an extraction.

A written diagnosis helps you compare the correct benefit category.

Ask the Dentist About Urgency

Some treatment can be completed in stages, while other problems should not be delayed.

Insurance considerations should not replace professional advice about infection, uncontrolled pain, swelling, trauma, or other urgent symptoms.

Request the Treatment Codes and Fees

The insurer can provide a more useful answer when you have the CDT codes and the dentist’s estimated charges.

Compare Immediate Insurance Benefits With Alternatives

A no-wait plan may be helpful, but it is not automatically the least expensive option.

Compare the expected insurance payment with the cost of the premiums, deductible and patient coinsurance. Also ask the dental office about payment plans, phased treatment, cash rates, office membership programs, community clinics, or discount plans.

Do Not Begin Treatment Before Confirming the Effective Date

Treatment performed before the effective date will generally not become covered simply because you later enroll.

Obtain confirmation that the policy is active and that your dentist participates in the correct network.

Who May Benefit From a No-Wait Dental Plan?

A no-waiting-period policy may be appropriate for someone who needs a covered filling, extraction, root canal, crown, denture, or other treatment soon and can receive enough first-year benefits to justify the premium and cost sharing.

It may also work for a person who wants to avoid future waiting periods and expects to keep the policy long enough to benefit from increasing annual maximums or coverage percentages.

People who value dentist flexibility may prefer a PPO, while those who want predictable copayments and have a suitable participating dentist may prefer a DHMO.

When a No-Wait Plan May Not Be the Best Choice

A no-wait plan may provide limited value when the required procedure is excluded, the first-year percentage is very low, the annual maximum is too small, or the necessary dentist does not participate.

It may also be unsuitable when the policy excludes treatment that has already started or a missing tooth that existed before enrollment.

Someone who needs only one procedure should compare the full first-year insurance cost against the expected benefit. Paying twelve months of premiums for a small insurance contribution may cost more than using a negotiated cash rate or discount program.

Questions to Ask Before You Enroll

| Question | Why it matters |

|---|---|

| What is the exact policy effective date? | No-wait benefits generally begin only after the policy is active. |

| Which services have no waiting period? | A plan may remove waiting periods for some services but not others. |

| Are preventive, basic and major services treated differently? | Each service category may have different benefit rules. |

| What is the first-year coverage percentage? | Some plans have no waiting period but pay a lower percentage during the first year. |

| Is there a deductible? | You may need to pay the deductible before benefits apply. |

| What is the annual maximum? | The plan may stop paying after it reaches the yearly benefit limit. |

| Is my dentist in network? | Network status can affect whether the plan applies and how much you pay. |

| Are there missing tooth clauses or treatment-in-progress exclusions? | These rules can affect services you already needed before enrolling. |

| Does the plan cover the exact procedure I need? | Procedure codes and service categories determine whether benefits may apply. |

| Can I get the answer in writing before treatment? | A written estimate or predetermination can help avoid surprises. |

Before enrolling, ask for the plan documents and confirm the details directly with the insurer or dental office. A plan may advertise no waiting period, but deductibles, annual maximums, exclusions and network rules can still affect your final cost.

💚Our Recommendation

The words “no waiting period” are only the beginning of the comparison.

Do not choose dental insurance based only on the words “no waiting period.” Begin with the dental treatment you are likely to need. Obtain the procedure codes and estimated fees from your dentist. Then compare plans based on the effective date, exact covered services, first-year coverage percentages, deductible, annual maximum, network access and treatment limitations.

For urgent major work, pay special attention to graded benefits. A plan with immediate eligibility and 20% first-year major coverage may be less useful than a copay plan with a strong local network or another option with a higher immediate benefit.

For fillings or simple extractions, a lower-cost plan covering basic services immediately may be sufficient. Paying for broad major-service coverage is unnecessary when the policy does not match your expected needs.

The goal is not to find a plan that merely uses the phrase “no waiting period.” The goal is to find a plan that provides meaningful first-year value for the treatment you actually need.

When you are ready to review options, compare dental plans based on effective dates, waiting periods, covered services, first-year benefits, annual maximums and dentist access.

Helpful Resources

🔥Our Editorial Standards

Dental Coverage Hub is committed to providing clear, educational and regularly reviewed information about dental plans and dental insurance.

Sources

HealthCare.gov — Dental Coverage in the Marketplace.

American Dental Association — Introduction to Dental Benefits.

Last reviewed: July 4, 2026. This article is for educational purposes only and is not dental, insurance, financial or legal advice. Plan benefits, provider networks, premiums, waiting periods and state availability can vary. Always review official plan documents before enrolling.

Frequently Asked Questions

Can I buy dental insurance today and use it immediately?

Possibly, but the plan must first become effective. A no-waiting-period policy may allow covered benefits to begin on the effective date, which is not necessarily the same day you submit the application. Confirm the effective date before receiving treatment.

Does dental insurance with no waiting period cover fillings?

Some plans cover fillings immediately because they are classified as basic services. You may still owe a deductible and coinsurance, and first-year coverage can be lower than later-year coverage.

Does no waiting period mean no deductible?

No. Waiting periods and deductibles are separate plan features. A plan can have no waiting period but still require an annual or one-time deductible before it begins paying for basic or major services.

Does no waiting period mean there is no annual maximum?

No. Many no-wait PPO plans still limit how much the insurer will pay during the first benefit year. Some DHMO and preventive plans do not use an annual maximum, but they may have network restrictions, copayments or limited covered services.

Will insurance cover a dental problem I already had?

It depends on the policy. A plan may cover treatment for an existing condition but exclude work that began before the effective date. Missing tooth clauses, replacement limits and other exclusions may also apply.

Can I use any dentist?

PPO plans may allow you to visit an out-of-network dentist, although your costs can be higher. DHMO plans generally require care from a selected primary dentist and participating specialists. Always verify the exact network before enrolling.

Is a dental discount plan better for immediate treatment?

It can be, depending on the procedure and available dentists. A discount plan may provide immediate access to negotiated rates without insurance waiting periods, but it does not pay claims. Compare the discounted fee with the total first-year cost and expected benefit of an insurance plan.

Does no waiting period mean full coverage?

No. A plan may have no waiting period and still use deductibles, coinsurance, copays, annual maximums, network rules, exclusions or lower first-year benefits. No waiting period only means an eligible service may be considered for benefits sooner.

About the Author: M.D.-Content creator and researcher focused on helping consumers better understand dental plans, coverage options and dental insurance concepts.

Reviewed by Dental Coverage Hub Editorial Team. Content is reviewed regularly to help ensure information remains accurate, practical and useful for consumers exploring dental coverage options in the United States.

✅ This article is intended for educational purposes only and should not be considered insurance, financial or legal advice.