🟢 Beginner Friendly

🟢 Dental Plan Basics

🟢 Updated 2026

Dental Insurance Basics: How Plans, Costs and Coverage Work

Dental insurance can feel confusing at first. This guide explains how dental plans work, what they may cover, which costs to compare and what to review before choosing coverage.

Quick Answer: What Is a Dental Plan?

A dental plan is a type of coverage or savings arrangement that may help reduce the cost of dental care.

Depending on the plan, it may help pay for preventive services such as exams, cleanings and X-rays, as well as basic or major treatments like fillings, extractions, crowns, dentures or root canals.

Most dental plans do not cover every service in full. They may include monthly premiums, deductibles, copayments, coinsurance, annual maximums, provider networks, waiting periods and service limits.

That is why understanding the basics first can make it easier to compare dental plans with confidence.

How Dental Insurance Plans Work

Dental plans are designed to help make dental care more predictable, but they do not all work the same way.

With traditional dental insurance, you usually pay a monthly premium to keep the plan active. When you receive dental care, the plan may help pay part of the cost for covered services, depending on the plan rules.

Most dental insurance plans use several basic features:

- Premium: The amount you pay to keep the plan active.

- Provider network: The dentists or specialists who participate in the plan.

- Covered services: The dental treatments the plan may help pay for.

- Deductible: The amount you may need to pay before certain benefits begin.

- Copayment or coinsurance: Your share of the cost for a covered service.

- Annual maximum: The most the plan may pay toward eligible services in a benefit year.

- Waiting period: A period of time before certain benefits become available.

Here is the basic process:

- You enroll in a dental plan.

- You choose a dentist, often from the plan’s network.

- The dentist provides a covered service.

- The service is categorized as preventive, basic, major or orthodontic care.

- The plan pays according to its rules.

- You pay any remaining cost, such as a deductible, copayment, coinsurance or amount above the annual maximum.

Some dental options, such as dental savings plans, work differently. Instead of paying insurance claims, they may give members access to reduced fees from participating dentists.

Because dental plans can vary, it is important to review the plan documents before enrolling. A plan summary can give you a quick overview, but the full details explain what is covered, what is excluded and what costs may remain your responsibility.

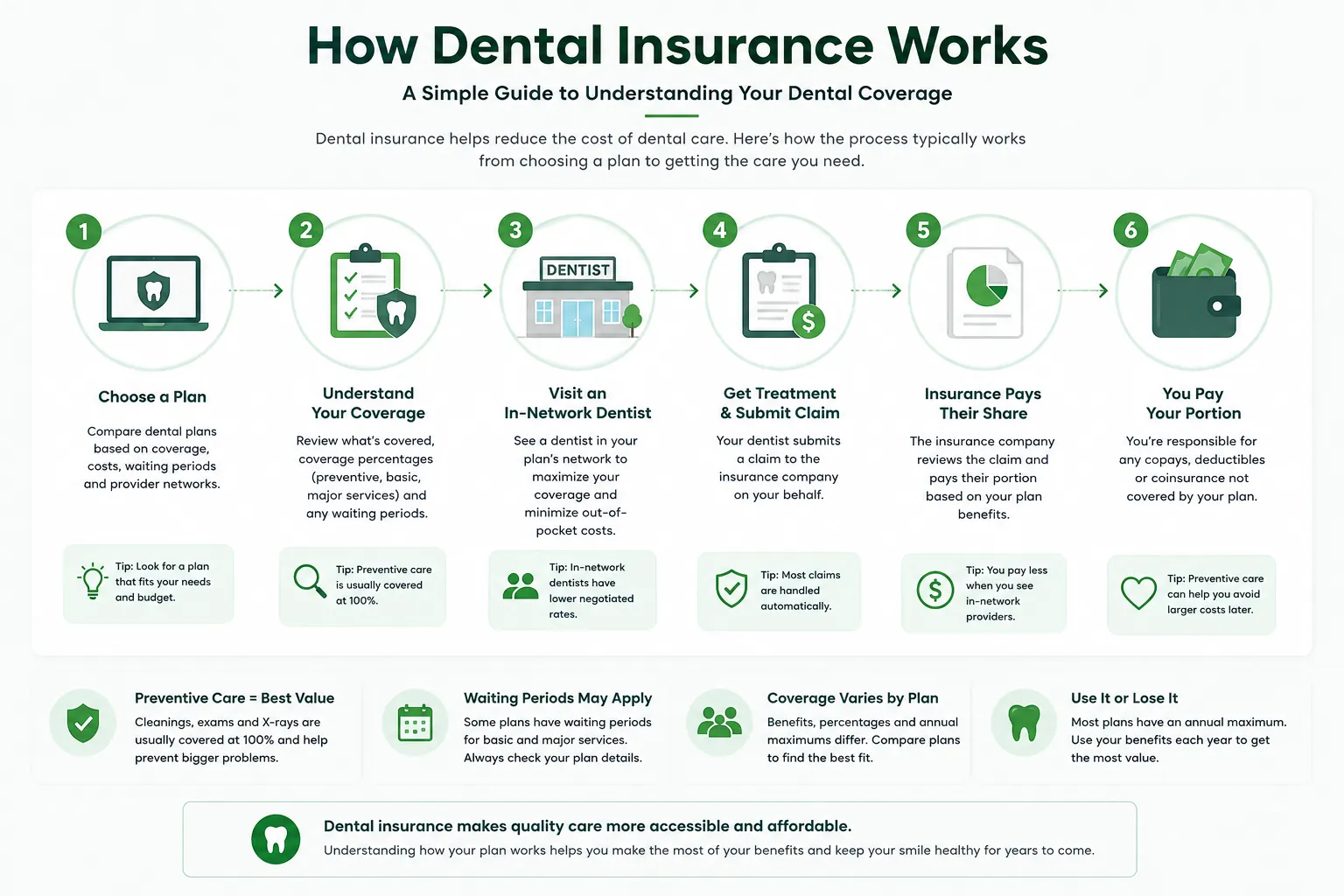

How Dental Insurance Works: Step-by-Step Overview

Simple infographic explaining how dental insurance works from enrollment to covered dental care and out-of-pocket costs.

Quick Takeaway

Dental insurance does not eliminate all dental costs. It can be more useful when you understand your coverage, review plan limits and compare options carefully.

Common Types of Dental Plans

Dental plans can be structured in different ways. The type of plan can affect which dentists you can visit, how costs are shared and how much flexibility you have when getting care.

The most common plan types include PPO dental plans, HMO dental plans, indemnity dental plans and dental savings plans.

PPO Dental Plans

A PPO dental plan usually gives members access to a network of participating dentists. These plans may also provide some out-of-network benefits, although using an in-network dentist may help lower costs.

PPO plans may be useful for people who want more provider flexibility, but premiums and out-of-pocket costs can vary by plan.

HMO Dental Plans

An HMO dental plan generally uses a more limited provider network. Members may need to choose a primary dentist or receive care from dentists who participate in the plan’s network.

HMO plans may have lower monthly premiums in some cases, but they usually offer less flexibility than PPO plans.

Review our PPO vs HMO Dental Plans guide to understand how these two plan types compare.

Indemnity Dental Plans

An indemnity dental plan may allow more freedom to choose a dentist, depending on the plan. Instead of requiring care through a narrow network, the plan may pay a set portion of eligible dental costs.

These plans can offer flexibility, but members should review reimbursement rules, covered services, deductibles, annual maximums and possible balance billing.

Indemnity dental plans are not always available in every area, and they may work differently from PPO or HMO plans.

Dental Savings Plans

A dental savings plan is not dental insurance. It is usually a membership program that provides access to discounted fees from participating dentists.

Instead of paying claims, a dental savings plan may reduce the price of certain services when care is received from a participating provider.

This option may be worth comparing for people who want an alternative to traditional dental insurance, but it is important to confirm which dentists participate and what discounts apply.

Review our Dental Insurance vs Dental Savings Plans guide before deciding which option better fits your needs.

What Dental Plans Usually Cover

Dental plans often group covered services into categories. These categories help determine how much the plan may pay and how much the member may owe.

The exact coverage depends on the plan. A service may be listed as covered, but it may still be subject to deductibles, copayments, coinsurance, annual maximums, waiting periods, provider network rules or frequency limits.

Preventive Care

Preventive care usually includes routine services that help maintain oral health and identify problems early.

Examples may include:

- Dental exams

- Teeth cleanings

- Dental X-rays

- Fluoride treatment

- Sealants for children, when included

- Routine checkups

Some plans may cover preventive services at a higher benefit level, but details vary by plan.

Learn more in our Preventive Dental Care guide.

Basic Care

Basic care usually includes common treatments for smaller dental problems.

Examples may include:

- Fillings

- Simple extractions

- Basic periodontal treatment

- Emergency pain relief

- Some diagnostic services

Basic services may be covered differently from preventive care. They may be subject to a deductible, coinsurance or waiting period.

Major Care

Major care usually includes more complex or expensive dental treatment.

Typical services include:

- Crowns

- Bridges

- Dentures

- Root canal treatment

- Oral surgery

- Some periodontal procedures

- Dental implants, when included

Major services often have more limitations than preventive care. A plan may use waiting periods, annual maximums, replacement limits, exclusions or lower coverage percentages for these treatments.

Orthodontic Care

Orthodontic care includes treatment that helps move or align teeth.

Examples may include:

- Traditional braces

- Clear aligners

- Retainers

- Orthodontic consultations

Orthodontic benefits are not included in every dental plan. When they are included, they may have age limits, lifetime maximums, waiting periods or separate coverage rules.

Before choosing a plan, review whether orthodontic care is included and whether the benefit applies to children, adults or both.

Common Dental Plan Costs

The monthly premium is only one part of the total cost of a dental plan.

Before choosing coverage, review how the plan handles premiums, deductibles, copayments, coinsurance, annual maximums and out-of-pocket costs.

Monthly Premiums

The monthly premium is the amount paid to keep the dental plan active.

A lower premium may look attractive, but it does not always mean the plan will cost less over the year. A lower-premium plan may have a smaller provider network, lower annual maximum, longer waiting periods or higher costs when care is used.

Compare the premium with the services you expect to need.

Deductibles

A deductible is the amount a member may need to pay before certain plan benefits begin.

Some plans may waive the deductible for preventive care, while applying it to basic or major services. Other plans may use different deductible rules.

Review whether the deductible applies per person, per family or per benefit year.

Copayments and Coinsurance

A copayment is a fixed amount paid for a covered service.

Coinsurance is a percentage of the cost that the member pays after the plan applies its benefits.

For example, if a plan covers part of a basic service, the member may still owe a percentage of the allowed cost, plus any deductible or non-covered charges.

Copayments and coinsurance can make two plans with similar premiums feel very different when dental care is actually used.

Annual Maximums

The annual maximum is the most a dental plan may pay toward eligible services during a benefit year.

After the plan reaches this limit, the member may be responsible for additional covered dental costs for the rest of that benefit year.

A higher annual maximum may be useful if major dental work is expected, but it should be compared with premiums, deductibles, coinsurance, waiting periods and covered services.

Out-of-Pocket Costs

Out-of-pocket costs are the amounts the member pays directly.

These may include:

- Premiums

- Deductibles

- Copayments

- Coinsurance

- Costs above the annual maximum

- Non-covered services

- Out-of-network charges

- Charges above the plan’s allowed amount

The lowest monthly premium is not always the lowest total cost. A better comparison looks at what the plan may cost over a full year, especially if dental treatment is expected.

Waiting Periods and Coverage Limits

Dental plans may include waiting periods, coverage limits and exclusions that affect when and how benefits can be used.

A waiting period is a period of time after enrollment before certain benefits become available. Some plans may make preventive services available sooner, while basic, major or orthodontic services may have longer waiting periods.

Waiting periods can be especially important if you already know you may need dental treatment soon.

Review our How Dental Insurance Waiting Periods Work guide to understand how waiting periods may affect preventive, basic, major and orthodontic care.

Some plans may advertise no waiting period for certain services. However, “no waiting period” does not always mean every procedure is covered immediately or at the highest benefit level.

If you need coverage you can use sooner, read our No Waiting Period Dental Insurance guide before choosing a plan.

Coverage limits can also affect how much a plan may pay.

Common limits may include:

- Annual maximums

- Frequency limits for cleanings or X-rays

- Replacement limits for crowns, bridges or dentures

- Age limits for orthodontic care

- Exclusions for certain procedures

- Network restrictions

- Prior authorization requirements

- Alternative benefit rules

Before enrolling, review the full plan documents, not only the summary. A service may appear to be covered, but the details determine when the benefit starts, how much the plan may pay and what costs remain your responsibility.

🔍 How to Choose a Dental Plan

Choosing a dental plan is easier when you compare the same factors across each option.

Start with your expected dental needs, then review the plan’s costs, network, coverage rules and limits.

1. Start With the Care You Expect to Need

Think about the dental care you or your household may use during the next year.

This may include:

- Routine exams and cleanings

- Dental X-rays

- Fillings

- Extractions

- Gum care

- Crowns or other major treatment

- Dentures or tooth replacement

- Orthodontic care

- Emergency dental visits

You do not need to predict every treatment perfectly. The goal is to understand whether you mostly need preventive care or whether basic or major services are likely.

2. Check Whether Your Dentist Is In Network

A dental plan may cost less when you use a participating dentist.

Before enrolling, confirm whether your current dentist participates in the plan’s network. If you do not have a dentist, review whether the plan has participating dentists near your home, work or school.

Do not rely only on a provider directory. Confirm participation with both the dental office and the plan before scheduling care.

3. Compare the Total Cost, Not Only the Premium

A low monthly premium does not always mean the lowest yearly cost.

Compare:

- Monthly premiums

- Deductibles

- Copayments

- Coinsurance

- Annual maximums

- Out-of-network costs

- Costs for non-covered services

A plan with a higher premium may still be a better fit if it provides stronger coverage for the services you expect to use.

4. Review Waiting Periods and Benefit Limits

Before choosing a plan, check whether any services have waiting periods or special limits.

Review:

- Waiting periods for basic, major or orthodontic care

- Annual maximums

- Replacement limits for crowns, bridges or dentures

- Frequency limits for cleanings or X-rays

- Orthodontic age limits

- Prior authorization requirements

- Exclusions

These details can affect how useful the plan is when you actually need care.

5. Match the Plan to Your Situation

The best dental plan for one person may not be the best plan for another.

A family may prioritize dependent coverage and orthodontic benefits. A retiree may focus more on major services, dentures or access to a preferred dentist. A self-employed person may compare individual and family coverage without employer benefits.

For broader guidance based on your situation, review our Dental Insurance by Life Stage guide.

6. Read the Plan Documents Before Enrolling

Plan summaries can be helpful, but they do not always show every detail.

Before enrolling, review the full plan documents, including:

- Covered services

- Exclusions

- Waiting periods

- Annual maximums

- Network rules

- Replacement limits

- Orthodontic rules

- Prior authorization requirements

- Member cost-sharing

If something is unclear, contact the plan, broker or dental office before enrolling.

📚Beginner Dental Insurance Guides

If you are still learning how dental insurance works, these guides explain the most important plan types, limits and cost questions in more detail.

Start with the topic that matches your biggest question, then return to this Dental Plans guide whenever you need the broader overview.

🟩 PPO vs HMO Dental Plans

Understand how PPO and HMO dental plans differ in provider flexibility, network rules and potential costs.

🟩 Dental Insurance vs Dental Savings Plans

Compare traditional dental insurance with dental savings plans so you understand how each option handles costs and provider access.

🟩 How Dental Insurance Waiting Periods Work

Learn why some dental benefits may not start immediately and what to review before scheduling treatment.

🟩 No Waiting Period Dental Insurance

Understand what “no waiting period” may mean, what it does not guarantee and which limits still matter.

🟩 Preventive Dental Care

Learn how routine exams, cleanings and X-rays may fit into dental coverage and why preventive care matters.

🟩 Is Dental Insurance Worth It?

Review when dental insurance may be useful, when limitations matter and how to think about total yearly value.

How Dental Plans Connect to Procedure Coverage and Life Stage Needs

After you understand the basics of dental plans, the next step is to look at how coverage may apply to your specific needs.

Some readers need to know whether a plan may help with a particular treatment, such as crowns, dentures, implants, braces or Invisalign. Others need to understand how dental coverage priorities may change for families, seniors, retirees, self-employed individuals or small business owners.

For treatment-specific questions, start with our Dental Insurance Coverage for Common Procedures guide.

For coverage needs based on your situation, start with our Dental Insurance by Life Stage guide.

These guides can help you move from general plan basics to the type of coverage questions that matter most for your own situation.

💚Our Recommendation

Before choosing a dental plan, take time to understand how the plan works rather than focusing only on the monthly premium.

Compare the plan type, provider network, covered services, deductibles, copayments or coinsurance, annual maximums, waiting periods and coverage limits. These details can affect how useful the plan is when you actually need care.

A good dental plan is not always the one with the lowest advertised cost. It is the one that best matches your expected dental needs, preferred dentists, budget and tolerance for out-of-pocket costs.

When you are ready to review options, compare dental plans using the same criteria across each plan so you can make a more confident decision.

📚 Helpful Resources

Continue learning with these beginner-friendly dental insurance guides:

- PPO vs HMO Dental Plans

- Dental Insurance vs Dental Savings Plans

- How Dental Insurance Waiting Periods Work

- No Waiting Period Dental Insurance

- Preventive Dental Care

- Is Dental Insurance Worth It?

- Dental Insurance Coverage for Common Procedures

- Dental Insurance by Life Stage

- Compare Dental Plans

- Dental Insurance Learning Center

Our Editorial Standard

DentalCoverageHub creates educational dental insurance content designed to help readers understand coverage before comparing plans.

Frequently Asked Questions About Dental Plans

What is a dental plan?

A dental plan is a type of coverage or savings arrangement that may help reduce the cost of dental care. Depending on the plan, it may help with preventive services, basic dental care, major treatment or orthodontic care.

What do dental plans usually cover?

Dental plans may cover preventive care such as exams, cleanings and X-rays, as well as basic or major services like fillings, extractions, crowns, dentures or root canal treatment. Coverage depends on the specific plan, service category, provider network and plan limits.

What is the difference between a PPO and HMO dental plan?

A PPO dental plan usually offers more provider flexibility and may include some out-of-network benefits. An HMO dental plan usually uses a more limited network and may require members to receive care from participating dentists. Costs and rules vary by plan.

Are dental savings plans the same as dental insurance?

No. Dental savings plans are not insurance. They are usually membership programs that provide access to discounted fees from participating dentists. Dental insurance generally uses premiums, covered-service rules and claims-based benefits.

Do dental plans have waiting periods?

Some dental plans may have waiting periods before benefits become available for basic, major or orthodontic services. Preventive care may be available sooner under some plans, but details vary.

What costs should I compare before choosing a dental plan?

Compare monthly premiums, deductibles, copayments, coinsurance, annual maximums, provider network rules, waiting periods and any costs for non-covered or out-of-network services.

How do I choose the right dental plan?

Start with the dental care you expect to need, then compare plan type, provider network, covered services, costs, annual maximums, waiting periods and exclusions. The right plan depends on your budget, preferred dentists and expected treatment needs.

Are dental plans worth it?

Dental plans may be worth it when the coverage helps with preventive care, lowers expected dental costs, includes dentists you can use and fits your yearly budget. The value depends on premiums, covered services, waiting periods, annual maximums, provider networks and the care you expect to need.

Ready to Compare Dental Plans?

Now that you understand the basics of dental plan types, costs, coverage categories, waiting periods and provider networks, you can compare options with more confidence. Review plan details carefully and compare dental plans based on your expected care needs, preferred dentists and total possible costs.